FHA Home Loans: Flexible Financing Solutions for Diverse Demands

FHA Home Loans: Flexible Financing Solutions for Diverse Demands

Blog Article

Home Loans Demystified: A Detailed Assessment of Loan Programs Tailored to Fit Your Monetary Circumstance and Goals

Navigating the landscape of home financings usually offers a daunting challenge, worsened by a myriad of programs designed to fulfill varied financial requirements. Comprehending the distinctions in between fixed-rate and adjustable-rate mortgages, as well as government-backed alternatives like FHA and VA lendings, is crucial for making educated decisions.

Comprehending Home Mortgage Basics

Although numerous people strive to homeownership, recognizing the basics of mortgage is critical to making educated economic decisions. A mortgage, also understood as a home loan, is a financial product that permits people to borrow money to purchase actual estate. The debtor is needed to pay off the car loan amount, in addition to interest, over a collection duration, usually ranging from 15 to three decades.

Secret elements of home financings consist of the principal, which is the quantity obtained, and the passion price, which determines the expense of borrowing. Lenders evaluate different variables, such as credit score rating, revenue, and debt-to-income proportion, to identify eligibility and finance terms. Furthermore, customers ought to know the relevance of down payments, which can affect finance approval and impact regular monthly payments.

Comprehending funding amortization is also necessary; this refers to the progressive decrease of the funding equilibrium in time through routine payments. By grasping these fundamental principles, possible home owners can navigate the mortgage landscape better, ultimately causing better economic end results and a more effective home-buying experience.

Kinds Of Mortgage

When checking out the landscape of home funding, recognizing the various types of mortgage is necessary for making an enlightened option. Home loan can mainly be classified right into fixed-rate and adjustable-rate home loans (ARMs) Fixed-rate home mortgages use a regular rate of interest and regular monthly repayment over the car loan's term, supplying stability, typically for 15 to thirty years. This predictability allures to homeowners that choose budgeting certainty.

Alternatively, ARMs have passion rates that vary based on market problems, typically beginning less than fixed-rate choices. However, these prices can adjust periodically, possibly enhancing monthly repayments gradually. Borrowers that expect relocating or refinancing before significant price adjustments may locate ARMs advantageous.

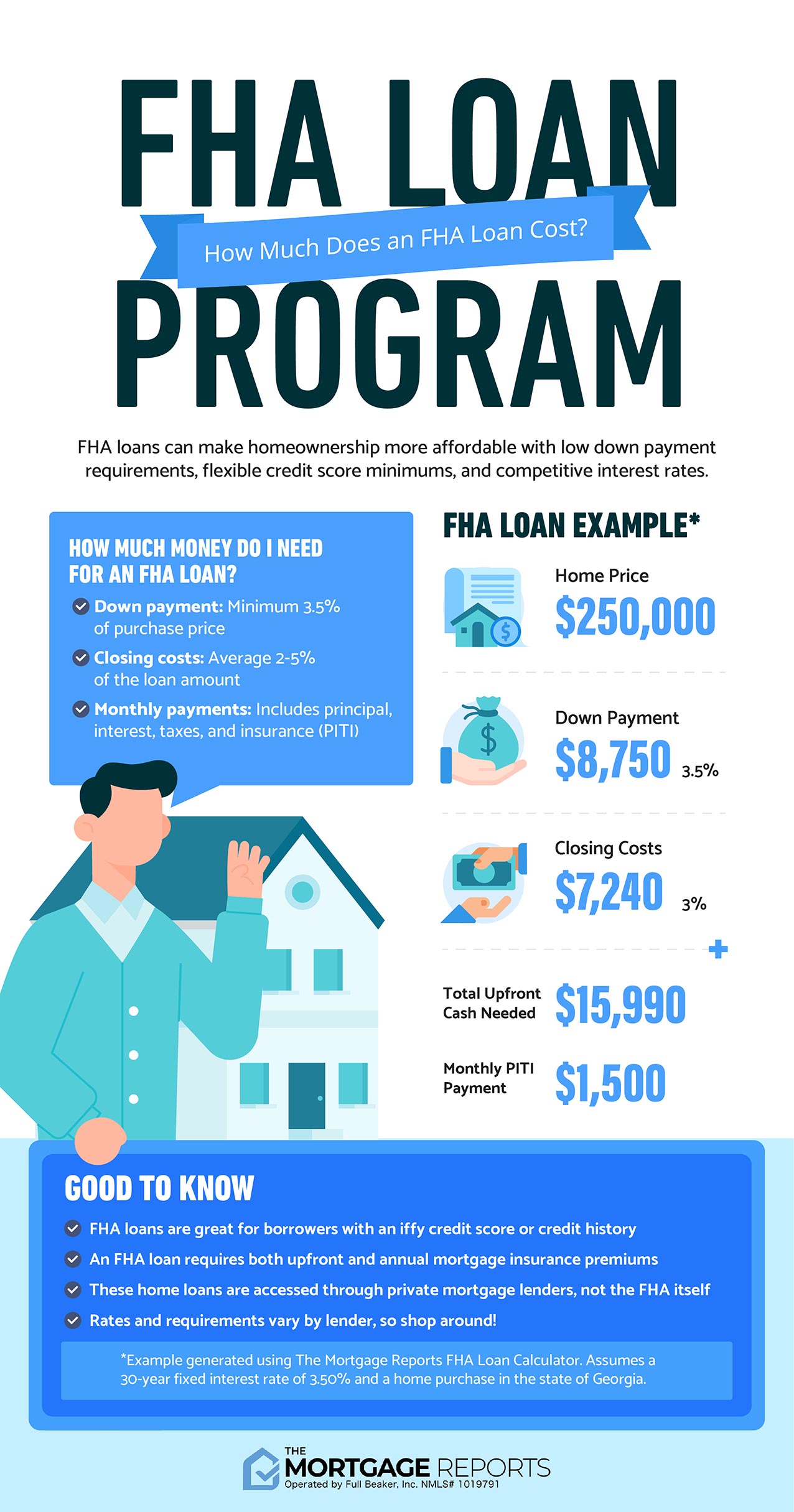

Additionally, government-backed lendings, such as FHA, VA, and USDA financings, provide to particular demographics and offer numerous advantages like reduced deposits and flexible credit rating demands. Conventional car loans, not insured by the government, frequently require higher credit history yet can give affordable rates for economically stable borrowers - FHA home loans. Understanding these finance types makes it possible for possible house owners to select the mortgage that lines up best with their financial situation and long-lasting goals

Key Eligibility Requirements

Navigating the qualification demands for a home mortgage finance is an essential step in the home-buying process. Understanding these requirements can dramatically simplify your application and improve your possibilities of approval.

The primary variables influencing eligibility include credit rating, income stability, debt-to-income (DTI) proportion, work history, and deposit quantity. Many lenders call for a minimum debt score of 620 for conventional finances, while government-backed financings may have more tolerant requirements. A secure income, showed through consistent work or self-employment documents, is essential for loan providers to analyze your capability to pay back the finance.

The DTI proportion, which contrasts your regular monthly debt repayments to your gross month-to-month revenue, normally must not surpass 43%, though some lending institutions might enable greater ratios in particular situations. In addition, the dimension of your deposit can affect qualification; while a larger deposit might enhance your chances, certain programs offer options for marginal visite site down repayments.

Finally, lending institutions will certainly review your general economic profile, including offered possessions and liabilities, to guarantee you are financially with the ability of preserving homeownership. Acquainting on your own with these key qualification demands will equip home you in the mortgage application journey.

Rate Of Interest Discussed

Recognizing the ins and outs of rates of interest is essential to making informed choices in the home lending procedure. Passion prices represent the price of borrowing cash and are expressed as a portion of the financing quantity. They can dramatically affect your monthly home mortgage repayments and the overall cost of your mortgage.

Rate of interest can be categorized right into taken care of and adjustable rates. Repaired prices continue to be constant throughout the funding term, giving predictability in monthly repayments. Alternatively, adjustable prices fluctuate based upon market conditions, which can lead to lower initial settlements but might enhance in time.

A number of elements affect rate of interest, consisting of the customer's credit history, financing term, and dominating financial conditions. Lenders evaluate these factors to determine the risk linked with lending to a certain borrower. Normally, a higher credit rating can lead to reduced rate of interest, while longer lending terms may cause higher prices.

Furthermore, broader financial indications, such as rising cost of living and financial plan, play a vital function fit rate of interest. Recognizing these elements enables debtors to much better navigate the lending landscape and select alternatives that straighten with their monetary objectives.

Choosing the Right Funding Program

Choosing the suitable loan program is essential for debtors intending to optimize their funding choices. With numerous funding kinds offered, including fixed-rate, adjustable-rate, FHA, and VA financings, understanding the nuances of each can dramatically affect long-term economic health.

Customers need to first examine their monetary situation, including credit history, income stability, and debt-to-income ratios (FHA home loans). A fixed-rate home loan provides predictability with regular regular monthly payments, suitable for those planning to remain in their homes long-term. On the other hand, variable-rate mortgages might supply lower preliminary rates, interesting buyers that expect relocating within a couple of years

Additionally, government-backed car loans such as FHA and VA choices can be advantageous for why not try these out novice homebuyers or professionals, as they usually call for reduced down settlements and have a lot more forgiving credit requirements.

Verdict

To conclude, navigating the complexities of home finances requires a complete understanding of numerous home mortgage programs and their unique functions. By assessing private economic situations and objectives, possible consumers can make informed decisions regarding the most ideal funding choices. Involving with a mortgage consultant can better promote this procedure, ensuring positioning in between personal situations and available finance programs. Ultimately, notified selections in home financing can cause improved monetary security and long-lasting fulfillment.

Fixed-rate mortgages supply a consistent interest price and monthly settlement over the loan's term, providing stability, often for 15 to 30 years.Additionally, government-backed loans, such as FHA, VA, and USDA fundings, cater to details demographics and supply various benefits like reduced down repayments and adaptable credit report demands. Many loan providers need a minimum credit report rating of 620 for standard loans, while government-backed loans might have much more lax criteria. Fixed prices remain constant throughout the finance term, giving predictability in regular monthly repayments. Usually, a higher credit scores rating can lead to reduced passion rates, while longer financing terms may result in higher rates.

Report this page